The System Is Failing, and Sometimes Making Things Worse

The scale of youth financial exploitation in the UK is now well-documented. What is less well-documented, and considerably more uncomfortable, is the degree to which the systems designed to address it are, in some cases, compounding the harm.

This is not a criticism of individuals within those systems. It is an observation about structural design, and it is one the anti-financial crime community has both the standing and the responsibility to engage with.

The criminalisation problem

When a financial institution identifies a young person’s account as exhibiting WUFE behaviour, the standard response is to de-bank the individual. That response is, in isolation, operationally reasonable. What it does not explore is whether the account holder is a victim.

Financial exploitation has a detrimental, long-term impact. In some cases, vulnerable people have had difficulty opening bank accounts and received criminal charges. The government recognises these children as victims. Yet the machinery of detection and reporting has not consistently reflected that recognition.

Cifas has acknowledged this tension explicitly. The reduction in WUFE cases filed in 2024 is partly explained by regulatory concern at the criminalisation of some vulnerable young people as a consequence of reporting. This has resulted in greater, and welcome, caution on the part of some organisations when filing cases involving young people. The fact that regulatory pressure was required to produce that caution is itself instructive.

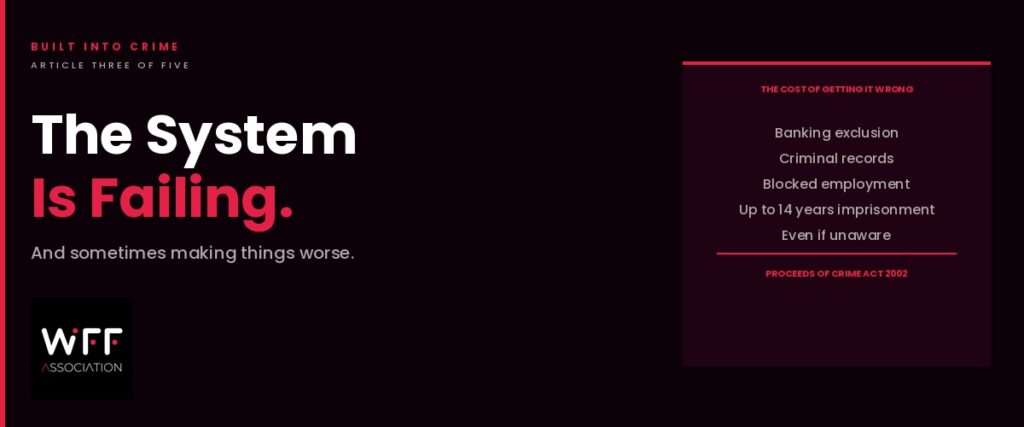

The practical consequences for a young person who has been exploited and then filed to the National Fraud Database can be severe and lasting. Account closure may follow, leaving them without basic banking access. A fraud marker can affect credit applications, employment prospects in financial services, and future account opening. A conviction can lead to job loss, especially in industries such as finance, law, and government. A poor financial record can impact credit scores, making it difficult to get mortgages, loans, or credit cards.

For a young person who was already financially vulnerable, which is a precondition of their recruitment, losing banking access can be catastrophic.

The legal exposure

The legal framework compounds this further. Those identified as having been involved in financial exploitation can be charged with money laundering, fraud, or aiding and abetting financial crime under the Proceeds of Crime Act 2002. Penalties can include up to 14 years in prison, even if the individual was unaware of the crime.

The phrase “even if the individual was unaware” is significant. It means that a 17-year-old who genuinely believed they were doing a favour for a friend, and who received a nominal payment for what they understood to be a legitimate transfer, is theoretically subject to the same criminal statute as the organised criminals who recruited them. In practice, prosecutorial discretion moderates this, but the legal architecture does not, by default, distinguish between perpetrator and victim.

When the victim is under 18 years old, financial exploitation is a form of child criminal exploitation. That framing, now embedded in government policy, has not yet fully permeated institutional practice.

Where institutions sit in no-man’s land

Financial exploitation of young people sits awkwardly between fraud, safeguarding, and criminal justice. No single institution owns it. And in that gap, young people frequently fall through.

Banks are not safeguarding bodies. Law enforcement is not a financial intelligence function. Educators are not equipped to identify the early signs of WUFE recruitment. And the data flows between these sectors remain, despite progress, limited.

The Home Office has committed to working with banks and local authorities to ensure vulnerable or exploited people are not removed from the banking system, developing a new protocol to make it easier for statutory services to notify a bank when someone is a victim of financial exploitation. That commitment exists. Its implementation is ongoing.

In the meantime, the 22-point Money Mule and Financial Exploitation Action Plan published by the Home Office in 2024 sets out cross-sector commitments from government, law enforcement, industry, and charities. The Home Office, UK Finance, and Cifas have developed educational materials for students, while the NCA and UK Finance have delivered online awareness campaigns aimed at those aged 18 and over. Law enforcement and banks have also supported Crooks on Campus in universities: a docudrama-based programme, developed by WFF, that uses fictional stories grounded in real cases to show students exactly how criminal recruitment operates and what the consequences of involvement look like. Piloted originally with the National Crime Agency, it produced significant awareness and behavioural change, with 90% of students rejecting financial exploitation recruitment messages after engaging with the programme. These are meaningful steps. But they remain fragmented, and the pace of criminal innovation continues to outstrip the pace of the response.

The research gap

Perhaps most significantly, the profession is working with incomplete information. Many young people who are exploited do not come forward. When they do, they may not be recognised as victims. The data that reaches the National Fraud Database, law enforcement, and academic researchers therefore reflects only a portion of what is actually occurring.

What practitioners need, and currently largely lack, is insight into the lived mechanics of exploitation: how grooming begins, how escalation happens, and how young people experience the transition from “easy money” to entrapment. Without that, both detection and intervention will continue to lag behind reality.

This is one of the central problems that TheCrooksProject.org is working to address, and which we will explore in Article Four.

For anti-financial crime professionals looking to engage meaningfully with the full complexity of financial crime, the WFFA provides the peer network, specialist knowledge, and cross-sector connections to make that possible.

Responses